When companies talk about mergers and acquisitions, the conversation usually revolves around tax treatment, valuation, and deal structure. What often gets overlooked—until it’s too late—is the 401(k) plan.

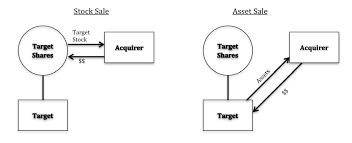

From a retirement plan perspective, the difference between an asset sale and a stock sale is not academic. It’s fundamental.

In a stock sale, the employer sponsoring the 401(k) plan stays intact. Ownership changes, but the company—and the plan—continue. Employees remain employees of the same legal entity, and the 401(k) plan generally rolls on without interruption.

In an asset sale, everything changes.

Employees typically terminate employment with the seller and are hired by the buyer. From a 401(k) standpoint, that means eligibility rules reset, service credit questions arise, and the seller’s plan often must be terminated or affirmatively merged. None of this happens automatically, and none of it fixes itself after closing.

This is where plan sponsors get burned.

I’ve seen deals labeled “tax-free reorganizations” where executives assumed the 401(k) plan would simply follow the business. It doesn’t work that way. ERISA doesn’t care how the deal is marketed. It cares who the employer is after the dust settles.

Failing to address this upfront leads to late enrollments, missed deferrals, improper plan terminations, and audit headaches that surface months—or years—later.

The takeaway for plan sponsors is simple: your 401(k) plan needs a seat at the deal table. HR, legal, payroll, and retirement advisors should be involved before documents are signed, not after employees start asking where their accounts went.

M&A transactions close fast. Retirement plan mistakes last a long time.